Table of Contents

Europe Diabetic Food Market Report Summary

The Europe diabetic food market was valued at USD 4.19 billion in 2025, increased to USD 4.42 billion in 2026, and is projected to reach USD 6.80 billion by 2034, growing at a CAGR of 5.53% during the forecast period. Market growth is primarily driven by the rising prevalence of diabetes, increasing health awareness among consumers, and growing demand for low-sugar, sugar-free, and functional food products. Supportive government initiatives promoting healthier diets, advancements in food formulation, and wider availability of diabetic-friendly products across organized retail channels are further accelerating market expansion across Europe.

Key Market Trends

Rising consumer shift toward sugar-free, low-GI, and functional diabetic food products to manage blood glucose levels.

Growing demand for diabetic confectionery products as manufacturers focus on taste parity with conventional sweets.

Expansion of private-label diabetic food offerings in supermarkets and hypermarkets, improving affordability and accessibility.

Increased use of natural sweeteners and clean-label ingredients to meet health-conscious consumer preferences.

Innovation in product formulations, including high-fiber, protein-enriched, and plant-based diabetic foods.

Segmental Insights

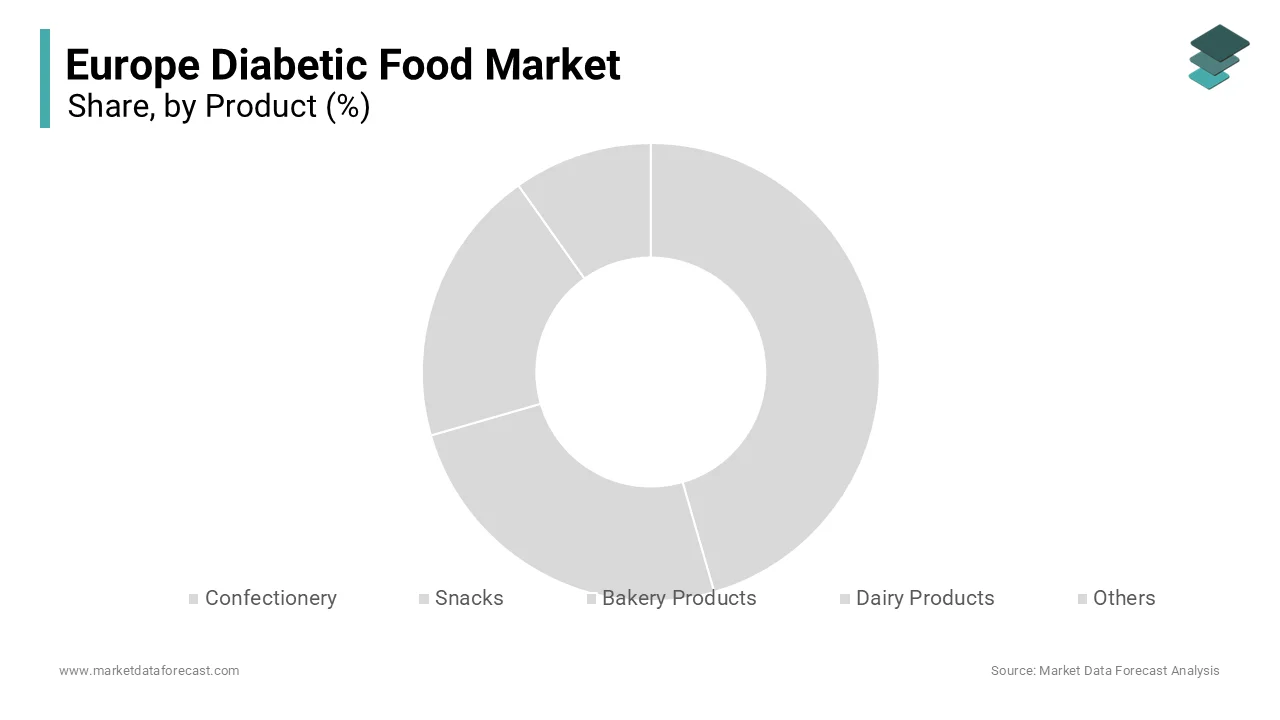

By product, the confectionery segment dominated the Europe diabetic food market by accounting for 57.5% of the market share in 2025, driven by strong consumer demand for sugar-free chocolates, candies, and snacks.

By distribution channel, supermarkets and hypermarkets held the largest share at 60.6% in 2025, supported by extensive product variety, competitive pricing, and strong consumer trust in organized retail formats.

Regional Insights

Europe continues to witness steady growth in the diabetic food market due to aging populations, lifestyle-related diabetes prevalence, and increasing preventive healthcare awareness.

Germany emerged as the largest market, accounting for 19.2% of the European diabetic food market share in 2025, driven by high health awareness, strong retail infrastructure, and early adoption of specialized dietary products.

Competitive Landscape

The European diabetic food market is moderately competitive, with global food giants and specialized health food manufacturers focusing on product innovation, clean-label formulations, and portfolio expansion. Leading players are investing in R&D, strategic partnerships, and retail penetration to strengthen their market presence. Key companies operating in the Europe diabetic food market include Nestlé, Unilever, The Kellogg Company, Conagra Brands, Inc., Fifty 50 Foods, Inc., Mars Inc., Tyson Foods, Sushma Gram Udyog, The Hershey Company, and Hain Celestial Group.

Europe Diabetic Food Market Size

The Europe diabetic food market size was valued at USD 4.19 billion in 2025 and is projected to reach USD 6.80 billion by 2034 from USD 4.42 billion in 2026, growing at a CAGR of 5.53%.

Diabetic food includes a distinct category of functional foods and beverages specifically engineered to support individuals managing diabetes mellitus. These products are formulated with reduced or modified sugars, elevated fiber content, and low glycemic carbohydrates to minimise postprandial glucose spikes. Unlike standard groceries, diabetic foods are developed in alignment with clinical nutritional guidelines, often incorporating alternative sweeteners such as erythritol, stevia, or maltitol, and functional ingredients like inulin or resistant starch. The European regulatory framework, governed by the European Commission and enforced through Regulation (EC) No 1924/2006, prohibits explicit health claims linking food to diabetes management unless scientifically validated and authorised by the European Food Safety Authority. As a result, marketing relies on neutral descriptors such as “no added sugar” or “low carbohydrate.” According to the International Diabetes Federation, 61 million adults in the European region lived with diabetes in 2023, which is creating a substantial and sustained need for dietary solutions that integrate seamlessly into daily life without compromising on taste or convenience.

MARKET DRIVERS

Rising Prevalence of Type 2 Diabetes Fuels Demand for Glycemic Control Foods

The escalating incidence of type 2 diabetes acts as the foremost driver of the European diabetic food market growth. According to the International Diabetes Federation, 61 million adults across the European region were living with diabetes in 2023, which is a figure expected to rise to 67 million by 2045. Nations such as Germany, Italy, and the United Kingdom exhibit adult diabetes prevalence rates exceeding 8%, compelling millions to adopt dietary strategies that mitigate glucose fluctuations. This clinical reality translates into consistent consumer interest in products that offer controlled carbohydrate release and minimal insulin response. Public health bodies, including Germany’s Federal Centre for Health Education and Public Health England, actively promote carbohydrate literacy and meal planning, indirectly endorsing the utility of low glycemic foods. Additionally, the integration of digital nutrition tracking tools has heightened awareness of macronutrient impact, prompting consumers to seek out foods explicitly designed for metabolic stability. Consequently, diabetic food manufacturers benefit from a convergence of medical necessity and proactive health behaviour, ensuring durable market relevance beyond transient wellness trends.

Growing Preventive Health Mindset Broadens Consumer Base

Beyond diagnosed patients, a pan-European cultural shift toward metabolic wellness and preventive nutrition is further boosting the European diabetic food market expansion. Even non diabetic consumers are increasingly conscious of sugar’s role in long term health, driven by both media discourse and policy initiatives. As per a 2024 survey by the European Food Information Council, 68% of European shoppers actively limit sugar intake, and 42% express concern about blood sugar regulation. This attitudinal evolution aligns with the European Union’s Farm to Fork Strategy, which mandates industry-wide sugar reduction in processed foods. Major retailers such as Carrefour and Tesco have responded by expanding private label offerings under wellness banners, effectively normalizing diabetic compatible foods as part of mainstream healthy eating. Social media further amplifies this trend, with nutrition influencers advocating balanced glycemic responses for sustained energy and weight management. By appealing to a wider audience seeking metabolic resilience, the diabetic food segment transcends its therapeutic niche and integrates into everyday dietary habits, significantly expanding its addressable market and fostering product trial among new demographics.

MARKET RESTRAINTS

Stringent EU Regulations Restrict Health Claim Communication

The European Union’s rigorous regulatory stance on nutrition and health claims represents a critical restraint for market growth. Under Regulation (EC) No 1924/2006, any claim suggesting a food’s benefit for diabetes management must undergo pre-approval by the European Food Safety Authority. To date, EFSA has not authorised any claim that explicitly links a food product to improved glycemic control in diabetics, rejecting numerous applications due to insufficient generalizability or inconsistent evidence. As per the European Commission’s official Nutrition and Health Claims Register, manufacturers are barred from labelling products as “suitable for diabetics” or implying therapeutic effects. This forces brands to rely on generic descriptors such as “sugar-free,” which lack clinical specificity and fail to convey functional relevance. According to a 2023 study in the European Journal of Clinical Nutrition, only 31% of consumers could accurately identify diabetes appropriate foods based on packaging alone. The resulting ambiguity undermines consumer trust and limits product differentiation, discouraging investment in innovation and stalling market expansion despite clear public health needs.

High Price Points and Uneven Distribution Limit Accessibility

The economic and logistical barriers associated with diabetic foods significantly constrain their adoption across diverse socioeconomic groups, which is another major restraint to the growth of the European diabetic food market. These products often carry premium pricing due to specialised ingredients and smaller production scales. According to a 2024 analysis by Germany’s Stiftung Warentest, diabetic labelled snacks and breakfast items cost 30 to 45% more than conventional equivalents. This price gap proves prohibitive for lower-income households, particularly in Southern and Eastern Europe, where out-of-pocket health expenditures remain high. Compounding the issue, physical availability is inconsistent; while urban centres in the Netherlands or Sweden offer dedicated diabetic aisles in pharmacies and supermarkets, rural regions often lack access. As per Eurostat data from 2023, 22% of Europeans in rural municipalities live more than 30 kilometres from a retailer stocking specialised dietary products. Furthermore, public healthcare systems across the EU do not reimburse diabetic foods, unlike pharmaceuticals or monitoring devices, leaving full cost responsibility with the consumer. This dual burden of cost and access restricts regular usage to a narrow segment of affluent or highly motivated individuals, capping market penetration and impeding volume-driven economies of scale.

MARKET OPPORTUNITIES

Growth of E-Commerce Enables Direct Consumer Engagement and Pan-European Reach

The digital transformation of food retail offers a strategic opportunity for the European diabetic food market. According to the European Electronic Commerce Association, online grocery sales in Europe grew by 18% in 2024, with health-focused categories experiencing accelerated adoption. E-commerce platforms allow niche diabetic food brands to bypass restrictive retail gatekeepers and engage consumers directly through personalised content, subscription models, and curated bundles. Companies such as Typsy in the United Kingdom and DiabFood in Germany utilise digital channels to deliver tailored meal plans based on user profiles, enhancing adherence and loyalty. Moreover, online marketplaces provide transparent nutritional information and peer reviews, addressing the trust deficit common in new product trials. Crucially, a single digital storefront can serve multiple countries, reducing the need for localised logistics and enabling rapid market entry. Social commerce on platforms such as Instagram further amplifies reach through dietitian-led demonstrations and real-time Q&A, fostering community and credibility. This digital infrastructure not only democratizes access but also generates actionable consumer insights, enabling agile product development and dynamic pricing aligned with regional preferences.

Convergence with Personalised Digital Health Ecosystems

The integration of diabetic foods into personalised digital health platforms presents a high-value opportunity for clinical validation and scalable delivery. According to the 2024 European Connected Health Alliance report, more than 12 million Europeans with diabetes now use digital tools such as continuous glucose monitors and AI-powered nutrition apps. These platforms collect real-time metabolic data, enabling hyper-customised dietary recommendations that often incorporate specific diabetic food products. Startups such as January AI and Lumen are pioneering algorithms that translate glycemic variability into precise food suggestions, creating demand for products formulated to exact nutritional specifications. Strategic partnerships with digital therapeutics providers further embed these foods into reimbursed care pathways; for example, Kaia Health in Germany includes curated diabetic snack boxes in its clinically validated type 2 diabetes program. Such collaborations shift the perception of diabetic foods from discretionary purchases to essential components of digital treatment protocols. As European healthcare systems increasingly adopt value-based reimbursement models that reward outcomes, the inclusion of tailored nutrition in digital care bundles could unlock institutional purchasing and sustainable revenue channels, elevating the market from retail novelty to an integrated therapeutic solution.

MARKET CHALLENGES

Regulatory Hurdles Delay Adoption of Next Generation Ingredients

Innovation in diabetic food formulation is hampered by the European Union’s cautious approach to novel ingredients and health claims, which is challenging the growth of the European diabetic food market. Despite global adoption of low glycemic sweeteners such as allulose, the European Food Safety Authority has not granted Novel Food authorisation for its use as of 2025, citing incomplete safety dossiers. Similarly, EFSA has consistently rejected health claims for functional fibres such as resistant dextrin due to methodological inconsistencies in submitted studies. According to a 2024 review by the European Federation of Food Science and Technology, only 2 out of 17 glycemic-related health claim applications since 2020 received positive scientific opinions. This regulatory inertia forces manufacturers to rely on older generation sweeteners such as maltitol, which can cause gastrointestinal discomfort and deter repeat purchases. The absence of harmonised definitions for terms such as “low glycemic” across member states further complicates cross-border marketing. Consequently, R&D investment remains subdued, and product portfolios stagnate, failing to meet evolving consumer expectations for clean label, natural, and physiologically compatible solutions. Until the approval process becomes more predictable and science-responsive, ingredient innovation will remain a bottleneck to product differentiation and consumer satisfaction.

Consumer Distrust of NonNutritive Sweeteners Hinders Product Acceptance

Public scepticism toward artificial and even some natural sweeteners isfurther challenging the expansion of the European diabetic food market. Despite EFSA’s repeated confirmations of safety within established limits, media narratives and social discourse have amplified concerns about long-term metabolic effects. According to a 2024 Eurobarometer survey, 57% of European consumers worry about regular sweetener consumption, linking it to gut dysbiosis and insulin resistance. This sentiment is especially pronounced among adults under 35. As per a 2023 study in the British Journal of Nutrition, 63% of younger consumers would avoid products containing non-nutritive sweeteners, even if recommended for diabetes. This perception gap forces manufacturers into a strategic dilemma: retain proven but controversial ingredients and risk market rejection, or adopt emerging alternatives such as monk fruit—facing supply constraints, high costs, and potential flavour challenges. The resulting reformulation difficulties delay product launches and increase development costs. Without coordinated scientific communication that bridges regulatory assurances and public understanding, this distrust will continue to limit trial, reduce brand loyalty, and obstruct the mainstream adoption of diabetic foods across diverse consumer segments.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

5.53%

Segments Covered

By Product, Distribution Channel, and Region

Various Analyses Covered

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

Nestlé, Unilever, The Kellogg Company, Conagra Brands, Inc., Fifty 50 Foods, Inc., Mars Inc., Tyson Foods, Sushma Gram Udyog, The Hershey Company, Hain Celestial Group, and others

SEGMENTAL ANALYSIS

By Product Insights

The confectionery segment led the market by accounting for 57.5% of the regional market share in 2025. The dominance of the confectionery segment in the European market is primarily attributed to persistent consumer demand for sugar-free indulgences that align with glycemic control without sacrificing taste or cultural eating habits. Chocolate, candies, and chewing gums formulated with non-nutritive sweeteners such as xylitol, erythritol, and stevia cater to both diagnosed diabetics and health-conscious individuals seeking to reduce sugar intake. According to the European Food Information Council’s 2024 Consumer Insights Report, 71% of European adults identify sweets as the most challenging food category to give up, which is creating sustained demand for diabetic compliant alternatives. Furthermore, confectionery items are widely available in pharmacies, supermarkets, and travel retail outlets, ensuring high visibility and impulse purchasing. The segment benefits from decades of formulation refinement, resulting in improved taste profiles and reduced gastrointestinal side effects compared to early-generation sugar alcohols. As per national diabetes associations in countries such as Germany and France, these products are indirectly endorsed in dietary guidance materials as occasional treats within a balanced meal plan. This combination of sensory satisfaction, accessibility, and partial clinical validation solidifies confectionery as the cornerstone of the diabetic food landscape in Europe.

The snacks segment is the fastest-growing category within the European diabetic food market and is anticipated to register a CAGR of 9.22% over the forecast period, owing to the convergence of lifestyle changes, product innovation, and shifting meal patterns across urban populations. As per data from Euromonitor International in 2025, 64% of European consumers now consume at least one snack between main meals, with protein and fibre-enriched options gaining particular traction among those managing metabolic conditions. Diabetic specific snack bars, savoury crackers, and baked chips formulated with chickpea flour, lupin protein, or resistant starch offer sustained satiety and minimal glucose impact, appealing to both diabetics and low-carbohydrate dieters. The rise of remote work and flexible schedules has further normalised frequent snacking, increasing the relevance of portion-controlled, on-the-go options. Additionally, manufacturers are leveraging clean label trends by eliminating artificial additives and emphasising plant-based ingredients, aligning with broader European consumer values. Retailers such as Edeka in Germany and Monoprix in France have dedicated shelf space to functional snacks under wellness banners, enhancing discoverability. Unlike confectionery, which is often viewed as discretionary, snacks are increasingly positioned as integral components of structured dietary management, enabling deeper integration into daily routines and driving consistent repeat purchases.

By Distribution Channel Insights

The supermarkets and hypermarkets segment accounted for 60.6% of the regional market share in 2025. The leading position of the supermarkets and hypermarkets segment in this regional market is attributed to the high footfall, established cold chain infrastructure, and consumer preference for tactile product evaluation before purchase. Major retail chains such as Carrefour in France, Tesco in the United Kingdom, and Albert Heijn in the Netherlands allocate dedicated sections within their health and wellness aisles for sugar-free and low glycemic products, enhancing visibility and normalising their consumption. According to the European Retail Round Table’s 2024 Retail Trends Report, 78% of European shoppers still prefer in-store grocery shopping for perishable and speciality items due to concerns over freshness and packaging integrity. Furthermore, supermarkets benefit fromlong-standingg relationships with national diabetes associations, often featuring co-branded educational materials that build trust. Promotional strategies such as loyalty card discounts and multi-buy offers also drive volume sales, particularly for household staple items like diabetic jams or breakfast cereals. The physical retail environment thus provides a credible, convenient, and sensory-rich experience that continues to anchor consumer behaviour despite the rise of digital alternatives.

The online distribution channel is the fastest-growing segment in the European diabetic food market and is predicted to witness a CAGR of 13.3% over the forecast period, owing to the digitisation of health management, rising demand for product variety, and logistical advancements that ensure reliable delivery of temperature-sensitive items. As per the European Electronic Commerce Association, online grocery penetration in Europe reached 11.4% in 2024, with health-focused categories growing twice as fast as the overall market. Platforms such as Amazon Pantry, Ocado, and specialised e-retailers like NutriActiv offer extensive catalogues of diabetic foods from both mainstream and niche brands, often accompanied by detailed nutritional breakdowns and user reviews that aid decision-making. Subscription models further enhance convenience, enabling automatic replenishment of frequently used items such as protein bars or sugar-free syrups. The integration of telehealth services has also accelerated adoption; digital diabetes coaching platforms in Sweden and the Netherlands now include curated food boxes as part of their care packages, delivered directly to patients’ homes. Crucially, online channels overcome geographical disparities, providing rural and underserved populations with access to products unavailable locally. This blend of personalisation, accessibility, and seamless integration with digital health ecosystems positions e-commerce as the most dynamic growth engine in the diabetic food distribution landscape.

REGIONAL ANALYSIS

Germany Diabetic Food Market Analysis

Germany dominated the diabetic food market in Europe in 2025 by holding 19.2% of the regional market share. The dominance of Germany in the European market is attributed to its high diabetes prevalence, robust healthcare infrastructure, and consumer receptivity to functional foods. According to the International Diabetes Federation’s 2023 Atlas, over 8 million adults in Germany were diagnosed with diabetes, representing one of the highest national burdens in Europe. The country’s statutory health insurance system covers diabetes education programs that emphasise dietary self-management, indirectly validating the role of specialised foods. German consumers demonstrate strong trust in scientifically backed nutrition, driving demand for products with transparent ingredient lists and clinically relevant formulations. Leading domestic brands such as Birkengold and Alnatura have pioneered sugar-free confectionery using birch-derived xylitol, while pharmacy chains such as dm drogerie markt dedicate prominent shelf space to diabetic snacks and beverages. Additionally, as per Germany’s Federal Ministry of Food and Agriculture, food reformulation initiatives under the National Reduction and Innovation Strategy encourage industry investment in low-sugar alternatives. This synergy between public health policy, retail infrastructure, and consumer literacy creates an exceptionally fertile environment for sustained market leadership.

United Kingdom Diabetic Food Market Analysis

The United Kingdom captured the second-largest share of the European diabetic food market in 2025. The growth of the UK in the European market can be credited to its agile regulatory environment and rapid adoption of digital health tools. As per Public Health England’s 2024 National Diabetes Audit, over 4.3 million people in the UK are living with diabetes, representing 7.8% of the adult population. The National Health Service’s embrace of digital therapeutics has catalysed integration between diabetic food products and remote care platforms; for instance, the NHS-endorsed digital program Low Carb Program includes partnerships with brands supplying low glycemic meal kits and snacks. British consumers are among the most receptive in Europe to clean-label and plant-based claims. According to a 2024 YouGov survey, 69% of UK consumers prioritise natural sweeteners such as stevia over synthetic alternatives. Retailers such as Boots and Holland & Barrett have expanded their diabetic ranges beyond traditional pharmacy confines into lifestyle wellness zones, supported by in-store dietitian consultations. Furthermore, post Brexit regulatory flexibility has enabled faster market entry for novel ingredients, giving UK-based startups a competitive edge in product innovation. This dynamic blend of clinical endorsement, consumer sophistication, and retail evolution positions the UK as a high-growth innovation hub within the European landscape.

France Diabetic Food Market Analysis

France occupied a notable share of the European diabetic food market in 2025. The growth of France in the European market is driven by its culinary heritage to develop premium, palatable diabetic products that align with national eating traditions. According to the French National Institute of Health and Medical Research, 4.5 million adults in France were diagnosed with diabetes in 2023, with rising incidence linked to ageing and obesity trends. Unlike other markets where diabetic foods are purely functional, French consumers expect sensory excellence, prompting brands such as La Pie qui Chante and Canderel to invest heavily in recipe refinement for sugar-free chocolates, biscuits, and dessert mixes. The country’s strong pharmacy distribution network ensures medically credible placement and pharmacist recommendations, building consumer confidence. Additionally, France’s National Nutrition and Health Program actively promotes carbohydrate awareness, indirectly supporting demand for low glycemic alternatives. The cultural emphasis on meal enjoyment, combined with high trust in pharmacist advice and state-backed nutritional guidance, creates a unique ecosystem where diabetic foods are not seen as compromises but as refined adaptations of classic gastronomy, sustaining premium pricing and brand loyalty.

Italy Diabetic Food Market Analysis

Italy is estimated to witness a healthy CAGR in the European diabetic food market during the forecast period due to its rapidly ageing demographic and increasing focus on preventive metabolic health. As per Istat, Italy’s National Institute of Statistics, 23.5% of the population was aged 65 or older in 2024, the highest proportion in Europe, and age is a key risk factor for type 2 diabetes. The Italian Ministry of Health reports over 4 million diagnosed cases, with an additional 1 million estimated to be undiagnosed, creating substantial latent demand for dietary support. Italian consumers, particularly seniors, favour familiar formats such as diabetic specific cookies, breakfast biscuits, and espresso-compatible sugar-free sweeteners that integrate seamlessly into daily rituals. Major food companies such as Ferrero and Barilla have launched low glycemic variants under sub-brands, capitalising on household name recognition. Pharmacies remain the primary point of discovery, but supermarkets such as Esselunga are increasingly featuring diabetic products in dedicated benessere aisles. Moreover, family-centred care models mean adult children often manage dietary purchases for elderly parents, prioritising ease of use and digestive tolerance. This intergenerational involvement, combined with high chronic disease burden, sustains steady consumption and drives product development toward mild formulations suitable for sensitive digestive systems.

Spain Diabetic Food Market Analysis

Spain is anticipated to account for a notable share of the European diabetic food market over the forecast period, with growth propelled by urban health consciousness, expanding retail modernisation, and public health campaigns targeting metabolic syndrome. According to the Spanish Ministry of Health’s 2024 National Diabetes Registry, 3.8 million adults live with diabetes, a 12% increase since 2019, largely attributed to sedentary lifestyles in major cities such as Madrid and Barcelona. Younger urban consumers are increasingly adopting low-sugar diets as part of fitness and wellness regimens, broadening the market beyond clinical patients. Retail chains such as Mercadona and Carrefour Spain have responded by launching private-label diabetic snack lines featuring Mediterranean ingredients such as almond flour and olive oil, aligning with regional dietary preferences. As per the Spanish Agency for Food Safety and Nutrition, sugar reduction is actively promoted through its Naos Strategy, which includes partnerships with food manufacturers to reformulate products. Additionally, the proliferation of nutrition influencers on Spanish social media platforms has normalised the consumption of sugar-free alternatives, particularly among women aged 25 to 45. This blend of policy support, retail responsiveness, and cultural alignment with local flavours is transforming Spain from a traditionally underpenetrated market into one of the fastest growing in Southern Europe.

COMPETITIVE LANDSCAPE

The European diabetic food market features a competitive landscape characterised by a mix of multinational nutrition companies, regional dairy specialists and agile health food startups. Incumbents leverage established distribution networks, clinical validation and brand trust to dominate pharmacy and supermarket channels. However, they face mounting pressure from niche players offering innovative clean-label formulations and direct-to-consumer models. Competition centres not only on glycemic performance but also on sensory appeal, digestive tolerance and alignment with broader wellness trends such as plant-based eating and gut health. Regulatory constraints prevent explicit medical claims, forcing differentiation through ingredient transparency, packaging design and digital engagement. Price sensitivity in Southern and Eastern Europe intensifies rivalry among value-oriented brands, while premium segments in Germany and Scandinavia reward scientific backing and personalisation. Continuous innovation in sweetener technology and fibre blends remains critical as consumer scepticism toward artificial ingredients grows. Ultimately, success hinges on balancing scientific rigour with everyday palatability across diverse national food cultures.

KEY MARKET PLAYERS

Some of the notable key players in the European diabetic food market are

Nestlé Unilever The Kellogg Company Conagra Brands, Inc. Fifty 50 Foods, Inc. Mars Inc. Tyson Foods Sushma Gram Udyog The Hershey Company Hain Celestial Group

Top Players in the Market

Nestlé S.A. maintains a significant footprint in the European diabetic food market through its science-driven medical nutrition portfolio under the Nestlé Health Science division. The company develops specialised oral nutritional supplements and low glycemic meal replacements tailored for individuals with impaired glucose tolerance. In recent years, Nestlé has intensified its focus onpersonalisedd nutrition by integrating digital health tools with its product offerings. It launched a range of functional snacks enriched with fibre and plant-based proteins designed to support metabolic health while aligning with European clean label expectations. Collaborations with endocrinology clinics and diabetes educators across Germany and France further reinforce its clinical credibility and consumer trust in therapeutic nutrition solutions. Danone S.A. contributes to the European diabetic food landscape primarily through its medical nutrition and plant-based dairy alternatives. Leveraging its Alpro and Fortimel brands, the company offers sugar-reduced yoghurt,s smoothies and clinical nutrition drinks formulated for glycemic control. Danone has recently invested in reformulating its product lines to eliminate artificial sweeteners in favour of stevia and monk fruit extracts, responding to rising consumer demand for natural ingredients. The company also partners with national diabetes associations in the United Kingdom and Spain to promote dietary awareness and integrate its products into nutrition counselling programs. These initiatives enhance its positioning as a provider of both everyday wellness and clinical support solutions. Zuivelgroep Nederland B.V. operates as aspecialisedd player focusing exclusively on diabetic friendly dairy products across the Benelux and German markets. Known for its DiaBalance brand, the company produces lactose-free yoghurt,s quark and drinkable yoghurts with low glycemic impact using natural fermentation and minimal added sweeteners. In 2,024 Zuivelgroep expanded its cold chain logistics network to ensure nationwide pharmacy and supermarket distribution while launching a digital platform offering personalised meal planning tools for diabetics. The company also engages in continuous dialogue with dietitians to refine product textures and macronutrient profiles, ensuring optimal digestive tolerance and patient adherence. This niche-focused strategy enables deep market penetration in regions with high diabetes awareness.

Top Strategies Used by the Key Market Participants

Key players in the European diabetic food market prioritise product reformulation to align with clean label and natural ingredient trends while ensuring glycemic efficacy. They actively collaborate with healthcare professionals and national diabetes organisations to build clinical credibility and integrate products into dietary management protocols. Investment in digital health ecosystems, includingpersonalisedd nutrition apps and telehealth partnerships, enhances consumer engagement anddata-driven personalisationn. Companies are expanding e-commerce capabilities to overcome retail shelf limitations and reach underserved rural populations. Strategic emphasis on sensory optimisation addresses historical taste and texture barriers associated with sugar-free products. Additionally, firms leverage private label development for major retailers to increase accessibility without compromising on formulation standards. Continuous consumer education through in-store dietitian programs and digital content combats misinformation around sweeteners. Sustainability in packaging and sourcing is increasingly incorporated to meet broader European consumer values beyond health functionality.

MARKET SEGMENTATION

This research report on the European diabetic food market has been segmented and sub-segmented based on categories.

By Product

Confectionery Snacks Bakery Products Dairy Products Others

By Distribution Channel

Supermarkets & Hypermarkets Specialty Stores Online Others

By Country

UK France Spain Germany Italy Russia Sweden Denmark Switzerland Netherlands Turkey Czech Republic Rest of Europe